15 April 2026

This article was commissioned by the Business Council of Co‑operatives and Mutuals (BCCM) as part of its work examining economic resilience and sovereign capability in Australia’s food and agricultural systems.

By Emeritus Professor Tim Mazzarol

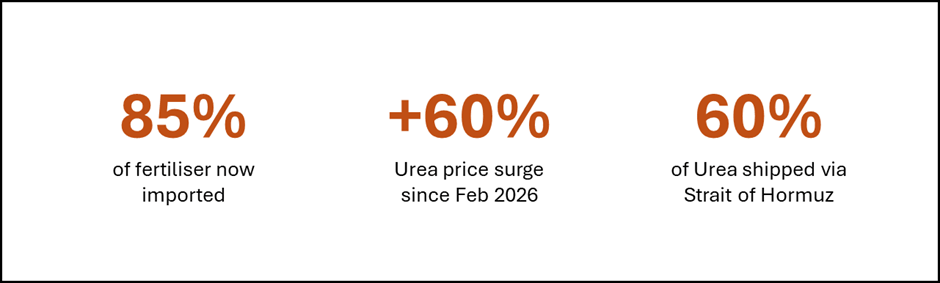

A century after farmer co‑operatives built a sovereign fertiliser industry from scratch, Australia now imports 85 per cent of what it needs – and a war in the Middle East is making the cost catastrophically clear.

The superphosphate that drove Australia’s wheat revolution was not imported. It was made here, by Australians, in factories built by farmer co-operatives who understood, in a way that their descendants apparently forgot, that a nation of nutrient-poor soils cannot afford to outsource its access to the one product that keeps those soils productive. Today, with urea prices more than doubling in a matter of weeks and half the country’s vegetable growers warning their stocks will run out before winter sowing is complete, the cost of that forgetting is landing on every farm in the country simultaneously.

Sources: Fertilizer Australia; Grain Central; Clime Capital Analysis (March 2026).

The current fertiliser crisis is not primarily a story about the Middle East, though the conflict there has been its trigger. It is a story about a century of industrial consolidation, co-operative dismantlement, and the quiet erosion of sovereign production capacity – a process that can be traced, with uncomfortable precision, through the history of the industry itself.

How Australia built its industry – and who built it

Large-scale fertiliser production in Australia began in 1875, when Cuming, Smith & Co. opened a superphosphate factory at Yarraville in Melbourne. Within a decade, production had spread to Adelaide and Port Melbourne. By the early twentieth century, Australia’s wheat farmers – working soils that agricultural scientists classify among the most phosphorus-deficient in the world – had adopted superphosphate almost universally.

Critically, the early supply chain was not simply a private-sector affair. After World War I, the governments of Australia, New Zealand and Britain jointly established the British Phosphate Commission to control mining on Nauru and Ocean Island, securing raw material for domestic manufacturers at preferential rates. State governments, particularly South Australia’s, erected tariff protection for local producers and ran their own subsidy programmes. The Commonwealth paid a superphosphate bounty under the Curtin government from 1941 and, after a political battle, reintroduced it in 1963 at $12 per tonne.

But the most striking feature of the industry’s formation was the role of farmer co-operatives. In Western Australia, Westralian Farmers’ Co-operative Ltd. – founded in 1914 by the state’s Farmers’ and Settlers’ Association – moved into direct fertiliser manufacture in 1927 through a three-way joint venture with Cuming Smith and Mount Lyell Mining. That entity, CSML, produced nearly two million tonnes of superphosphate in its first twenty years and supplied almost all of Western Australia’s requirements. In Victoria, the Phosphate Co-operative Company of Australia (later Pivot) was established in 1919 by farmers seeking to break the pricing power of commercial manufacturers. In Queensland, Australian Co-operative Fertilizers was doing the same from Toowoomba from 1915.

Key timeline

- 1875: first Australian superphosphate factory opens at Yarraville, Melbourne – Cuming, Smith & Co.

- 1914–1919: Westralian Farmers’ Co‑operative and Victorian Phosphate Co‑operative founded – farmers build their own supply chains

- 1941–1974: Commonwealth superphosphate bounty subsidises domestic use; withdrawn by the Whitlam government in 1974, causing a measurable decline in application rates

- 1979–1984: Wesfarmers acquires CSBP in Australia’s largest‑ever corporate takeover ($60 million); the co‑operative converts to a public company

- 2003: last major eastern co‑operative, Pivot, merges with Incitec to form Incitec Pivot – listed on the ASX; the co‑operative era ends

- 2021: China restricts urea exports; Australia nearly runs out of AdBlue for trucks – first modern sovereign supply crisis

- 2026: Strait of Hormuz disrupted; urea prices surge 60 per cent; half of Australia’s vegetable growers report impending shortages

The long dismantlement

The transition from co-operative model to corporate model was not sudden. It was a decades-long process, accelerated by the logic of financial markets and enabled by the assumption – reasonable in calmer times – that global supply chains were a perfectly adequate substitute for domestic production. Wesfarmers converted from co-operative to listed company in 1984. Pivot, the last of the great farmer-owned fertiliser enterprises, merged with Incitec Fertilizers in 2003. By the time that merger was complete, the industry’s co-operative roots were largely historical footnotes.

“In 2024, Australia consumed 8.7 million tonnes of fertiliser valued at A$5.5 billion – yet domestic production had declined to just 1.3 million tonnes, a mere 15 per cent of total consumption” (Paul Zwi, Clime Capital analyst, March 2026).

The consolidation that followed corporate listing was relentless. CSBP absorbed its rivals. Incitec Pivot absorbed Southern Cross Fertilisers from BHP in 2006, then Dyno Nobel in 2008. By 2025, Incitec Pivot was selling its fertiliser operations entirely, rebranding as Dyno Nobel Limited to focus on explosives – a final, ironic confirmation that the co-operative ambition of keeping farmers supplied with affordable nutrients had been fully superseded by shareholder value logic.

Meanwhile, the Gibson Island plant in Brisbane – once the centrepiece of eastern Australia’s nitrogen production – closed to fertiliser manufacturing in the early 2020s, killed by expensive gas. Australia’s domestic production fell to 15 per cent of consumption. The nation that had once built an entire sovereign phosphate supply chain now produced barely one tonne in seven that it used.

A co‑operative exception: CBH Fertiliser

Not every co-operative surrendered. One conspicuous exception to the story of dismantlement is Co-operative Bulk Handling Ltd. (CBH), the grower-owned grain handling co-operative that dominates Western Australia’s grain supply chain. While the eastern states’ co-operative fertiliser enterprises were converting to public companies or merging into listed corporations, CBH was moving in the opposite direction – entering the fertiliser market as a supplier precisely because its members could not afford for it to stand aside.

The importance of fertiliser to WA grain farmers is difficult to overstate. Due to the generally poor quality of WA soils – phosphorus-deficient, fragile, and heavily reliant on trace element supplementation – farmers in the state had depended on superphosphate from as early as 1894. The rapid development of WA agriculture after 1950 was closely tied to the large-scale application of fertiliser, which consistently accounted for over 30 per cent of total farm expenditures. When the Whitlam government removed the Commonwealth superphosphate bounty in 1974, withdrawing a subsidy of $12 per tonne, the reaction in WA was explosive: more than 6,000 farmers protested at Subiaco Oval, and Prime Minister Whitlam was pelted with tomatoes and soft drink cans at a Perth political rally. The message was unambiguous — for WA grain growers, fertiliser was not a discretionary input.

In 2015, CBH established CBH Fertiliser, operated through its subsidiary CBH (WA) Pty Ltd. The stated rationale was direct: the WA fertiliser market was dominated by only two major suppliers, pricing was opaque, and members were paying more than they should. As CBH Chief Executive Ben Macnamara explained:

“There were two key players in the market and there was limited transparency around pricing. And our desire was to provide transparency to our members around what they should be paying for fertiliser and avoiding potential market failure … what we’re trying to do is create a ceiling price and provide growers with transparency on what they should be paying so that even if they don’t buy the fertiliser from us, they can challenge the incumbent to provide them with a better price.”

This was co-operative logic applied with precision: not simply to sell product, but to discipline the broader market pricing structure to the benefit of members.

The enterprise grew rapidly. CBH Fertiliser sold 55,000 tonnes in 2016, its first full year of operation. By 2020 that figure had reached 125,000 tonnes, and in 2021 – a year of significant global fertiliser market disruption – sales reached 184,000 tonnes, representing a 41 per cent increase in new customers in a single year. CBH’s long-term strategy to 2033 targets a 15 per cent share of the WA fertiliser market. The co-operative also invested in bulk fertiliser storage infrastructure to support the distribution model.

It is important to note what CBH Fertiliser is and is not. It operates as a trading and supply business – sourcing fertiliser and on-selling it to members – rather than as a manufacturer. CBH has not, to date, constructed or operated fertiliser production facilities of its own, although it does undertake some blending. The historical manufacturing role in WA was played by entities such as Cumming Smith & Mount Lyell Farmers Fertilisers Ltd., which operated a superphosphate factory at Albany, and the broader CSML joint venture with Westralian Farmers’ Co-operative. CBH’s role has always been on the consumption side of the industry, and this remains the case. However, what it has done is use its collective purchasing power to reintroduce competitive discipline into a market that had become insufficiently competitive — precisely the role that the original farmer-owned co-operative fertiliser enterprises played a century earlier.

In the context of the current crisis, CBH Fertiliser’s existence provides its members with a degree of pricing protection and supply chain transparency that the broader national market lacks. It does not solve the structural problem of import dependence – CBH, like every other Australian fertiliser business, sources product from international markets. Nevertheless, it demonstrates that the co-operative model retains relevance as a mechanism for managing market power asymmetries, even when the co-operative in question is not a manufacturer. It is also a reminder that not all of the institutional knowledge built up during the co-operative era has been lost.

Why Australia is running short right now

The immediate cause is geopolitical. However, the vulnerability was structural and pre-existing – and those who built it deserve scrutiny. Australia has known about this risk since at least 2021, when China’s restriction on urea exports almost shut down the national road freight system by cutting off AdBlue supplies. The government introduced emergency measures at the time and promised to diversify supply chains. What followed was five years of slow progress and one planned urea plant – the Perdaman facility at Karratha – that will not be operational before 2027 at the earliest.

The structural causes are several. First, import dependence: with domestic production at just 15 per cent of consumption, Australia has no buffer when global supply is disrupted. Unlike oil, there are no internationally coordinated strategic reserves for fertiliser and no government stockpile to release. Second, geographic concentration: Australia imports 3.7 million tonnes of urea annually, the vast majority from Middle Eastern Gulf producers, with a secondary concentration in China – which has its own export restrictions in place. Third, market structure: the Australian fertiliser market is oligopolistic, with limited competition among importers amplifying international price shocks. Fourth, infrastructure: the barriers to entry for new importers – terminal capacity, storage, distribution – are high, locking in existing supply relationships even when those relationships become untenable.

The National Farmers Federation president Hamish McIntyre has called the emerging situation “extremely worrying.” Grain Growers chief executive Shona Gawel has warned of “serious ramifications” for Australia’s 2026 grain harvests. TasFarmers has written to the Australian Competition and Consumer Commission (ACCC) alleging price gouging. Tasmania has received what it describes as its “last foreseeable delivery” of urea. Vegetable growers across the country report stocks running out within weeks.

The Strait of Hormuz crisis

Conflict involving Iran has effectively closed one of the world’s most critical maritime chokepoints.

Approximately 20–30 per cent of global fertiliser supply, including urea, ammonia and phosphate, is produced in Middle Eastern countries that ship through the Strait. Approximately 60 per cent of Australia’s urea imports travel this route. Nearly one million metric tonnes of fertiliser cargo are physically stranded in the Gulf. Major producers have declared force majeure. Future shipments have been cancelled.

Urea prices have surged from approximately A$850 per tonne in late February 2026 to over A$1,400 per tonne in early April, an increase of more than 60 per cent in six weeks.

What history teaches – and what was ignored

The co-operative farmers who built this industry understood something that their successors forgot: that a country farming phosphorus-deficient soils in a continent distant from global supply chains cannot treat fertiliser as just another traded commodity. They built their own supply chains, lobbied for state support, accepted government partnership, and structured their enterprises to serve farmer members rather than financial markets.

That model was dismantled not by any single decision but by a cumulative logic of corporatisation, financialization and the confident assumption of globalisation. The Whitlam government removed the superphosphate bounty in 1974. The co-operatives converted to public companies in the 1980s. Domestic nitrogen production became uneconomic in the 2000s. The Gibson Island plant closed in the early 2020s. Each step was rational on its own terms. The aggregate result is a country that – despite a domestic population of only 27.5 million – exports roughly 70 per cent of its agricultural production and produces enough food to feed an estimated 60 to 80 million people worldwide grows food on soils that cannot grow without regular nutrient supplementation, relying for 85 per cent of that supplementation on imports routed through a single maritime chokepoint.

The Perdaman Karratha plant – a US$4.5 billion investment backed by a 20- year Woodside gas agreement – is the right idea, finally, a generation late. In the meantime, Australian farmers are being asked to plant a winter crop in an environment where the ratio of input cost to output revenue has made doing so, for many, financially irrational. The co-operative farmers of 1914 built an industry to prevent exactly that outcome. Their descendants are now living with the consequences of having dismantled it.

Sources and References

Australian Fertiliser Services Association (AFSA). “Our History.” https://www.afsa.net.au/about-us/our-history

Blainey, G. (1970). The Peaks of Power: A History of ICI in Australia. Melbourne University Press.

Byerlee, D. (2021). The Super State: The Political Economy of Phosphate Fertilizer Use in South Australia, 1880– 1940. Economic History Yearbook, 62(1): 99-128. https://doi.org/10.1515/jbwg-2021-0005

CSBP. “History.” https://www.csbp.com.au/about-us/history

Fertilizer Australia (2026). Australian Fertiliser Market. www.fertilizer.org.au/about-fertilzer

Fertilizer Australia (2026). letter to Minister for Agriculture, (2026, March 17). www.fertilizer.org.au

Fertilizer Industry Federation of Australia / Department of the Environment. Case Study 8: Fertilizer Industry Federation of Australia. Canberra: Australian Government. https://www.dcceew.gov.au

Government of South Australia – Primary Industries and Regions SA. “Farming systems – History of Ag SA.” https://pir.sa.gov.au/aghistory/industries/cereals_and_grains/wheat/farming_systems

Hancock Agriculture, “Nation comes a cropper as fertiliser crisis escalates,” March 2026

Incitec Pivot Fertilisers (2026). “Strategies to maximise in field nitrogen use efficiency amid global supply uncertainty” (2026, March 31). www.incitecpivotfertilisers.com.au

Incitec Pivot Fertilisers. “History.” https://www.incitecpivotfertilisers.com.au/about-us/history/

Kragt, M. (2026). Winter crops need to be sown. The Conversation, (2026, April 2). University of Western Australia.

Lockhorst, R. (2025). “Just like fuel, fertiliser supply chains are a hidden vulnerability,” (2025, March). The Strategist, Australian Strategic Policy Institute (ASPI), https://www.aspistrategist.org.au

Mazzarol, T. van Aurich, A., and Baskerville, B. (2024). Co-operative Bulk Handling Group Ltd. – Handling the Future and Growing Together, CEMI-CERU Case Study Research Report, CSR 2401, www.cemi.com.au and www.ceru.au Centre for Entrepreneurial Management and Innovation, and Cooperative Enterprise Research Unit. www.ceru.au

Parliament of Australia, Senate Select Committee on Agricultural and Related Industries. Inquiry into the Availability and Affordability of Agricultural Inputs (Interim Report, Chapter 2), 2009. https://www.aph.gov.au/Parliamentary_Business/Committees/Senate/Former_Committees/agric/completed_inquiries/2008-10/fertiliser/

Parliament of Australia. Hansard, Phosphate Fertilizers Bounty Bill 1963 (Second Reading), 28 October 1963. https://parlinfo.aph.gov.au

Parliament of Australia: Hansard, Phosphate Fertilizers Bounty Bill (1963); Fertilizers (Bounty and Subsidy) Amendment Bill (1982).

Russell, J. S. & Williams, C. H. (1982). Pasture Production and Fertiliser Use in Australia. CSIRO, Commonwealth of Australia.

TasFarmers media release (2026)., “Towards the gates of a recession,” (2026, March 13). TasFarmers www.tasfarmers.com.au

Tolley, M. (2026). “Fertiliser Food Freight Crisis Australia 2026,” (2026, April). Trace Consultants, www.traceconsultants.com.au

Weekly Times (1876). “Disastrous fires at Footscray”, (1876, September 16). Weekly Times, p. 7. www.trove.nla.gov.au

Wells, L. (2026). Fertiliser body seeks govt help to ease shortage. (2026, March 25). Grain Central. www.graincentral.com

Wesfarmers. “Our History.” https://www.wesfarmers.com.au/who-we-are/our-history

Williamstown Advertiser (1877). “Messrs. Cumin, Smith & Co. Chemical works Footscray”. (1877, August 25). Williamstown Advertiser, p. 3.

Zwi P. (2026). “Critical Vulnerability: Australia’s Fertilizer Supply,” (2026, March). Clime Capital.

About the author

Tim Mazzarol is an Emeritus Professor and Senior Honorary Research Fellow at the University of Western Australia. He is also the Director of the Centre for Entrepreneurial Management and Innovation (CEMI), an independent initiative designed to enhance awareness of entrepreneurship, innovation, and small business management. He is also the founder Director of the Co-operative Enterprise Research Unit (CERU), a special research entity for the study of co-operative and mutual enterprises (CMEs) at the University of Western Australia. Tim is also a Qualified Practising Researcher (QPR) as recognised by the Australian Research Society (ARS). He has around 20 years of experience of working with small entrepreneurial firms as well as large corporations and government agencies. He is the author of several books on entrepreneurship, small business management and innovation. He holds a PhD in Management and an MBA with distinction from Curtin University of Technology, and a Bachelor of Arts with Honours from Murdoch University, Western Australia.

Latest news

Co-ops and Mutuals poised to build a more resilient economy for Tasmanians

Parliamentary Friends reception showcases the national importance of producer co‑operatives