BCCM National Affordable Housing Strategy

Articulating the housing problem

Australia’s affordable housing crisis threatens the foundations of our social cohesion and standard of living. Increasing numbers of Australians, including many members of Australian co-ops and mutuals, face a widening wealth gap because they cannot get onto the housing ladder. Many more are impoverished both financially and socially by their lack of access to affordable rental accommodation. As a socially purposed business model, co-ops and mutuals arguably have a responsibility to provide solutions within our control.

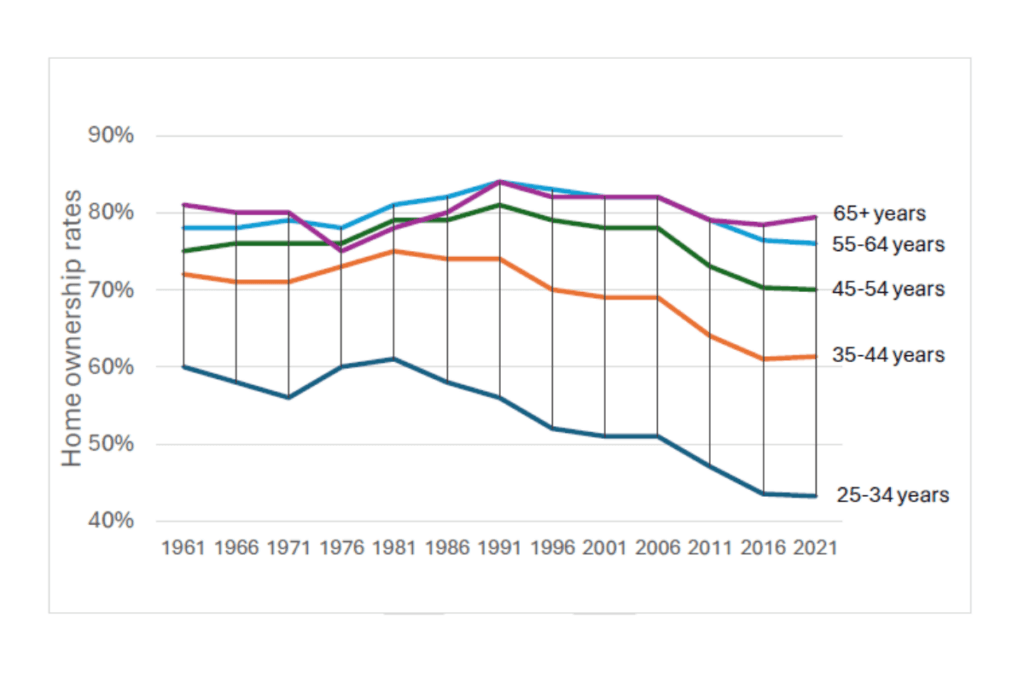

Australia has a shortage of affordable housing[1] with secure tenure where people have agency over their lives. The proportion of Australians who own their own home is declining.

Not owning a home (and thus relying on the private rental market) is linked to poverty, especially in retirement years. Further, insecure and unaffordable housing is linked to poorer health and lower quality of life. The chart below shows the decreasing rates of home ownership from 1961 to 2021. This is impacting younger people in particular.

Context – housing as unfinished business

Co-operatives and mutuals have a long tradition of responding to critical needs and market failure.

In the past, the sector has formed new housing finance models such as permanent building societies (1870s–1970s) and co-operative housing societies (which peaked in the1950s).

Compared to other authorised deposit-taking institutions, customer-owned banks have a higher share of lending to owner-occupiers at 77 per cent (versus 67 per cent) and first-home buyers at 20 per cent (versus 16.5 per cent). The sector has a deep heritage and an ongoing focus on mortgage lending, and it plays a significant role helping Australians own the home they live in.[3]

Housing co-operatives have operated in Australia since the 1880s. Dedicated government funding for rental housing co-operatives was available from the 1980s–1990s when the current sector was largely established. The original vision was to grow a rental housing co-operative sector in Australia extensive enough to be a mainstream option. Fulfilling this vision is unfinished business.

Central to housing co-operatives in Australia is ACHA[4], the Australian Co-operative Housing Alliance, a network of the largest rental housing co-operative bodies in Victoria, New South Wales, South Australia and Western Australia, and independent rental housing co-operatives in Victoria. ACHA advocates for the housing co-operative model and the growth and diversification of social housing in Australia. The BCCM has provided secretariat support to ACHA.

Housing co-operatives exist in each state and territory except the NT, although some First Nations homelands communities operate housing that is akin to the co-operative model.

The role of housing co-operatives in Australia

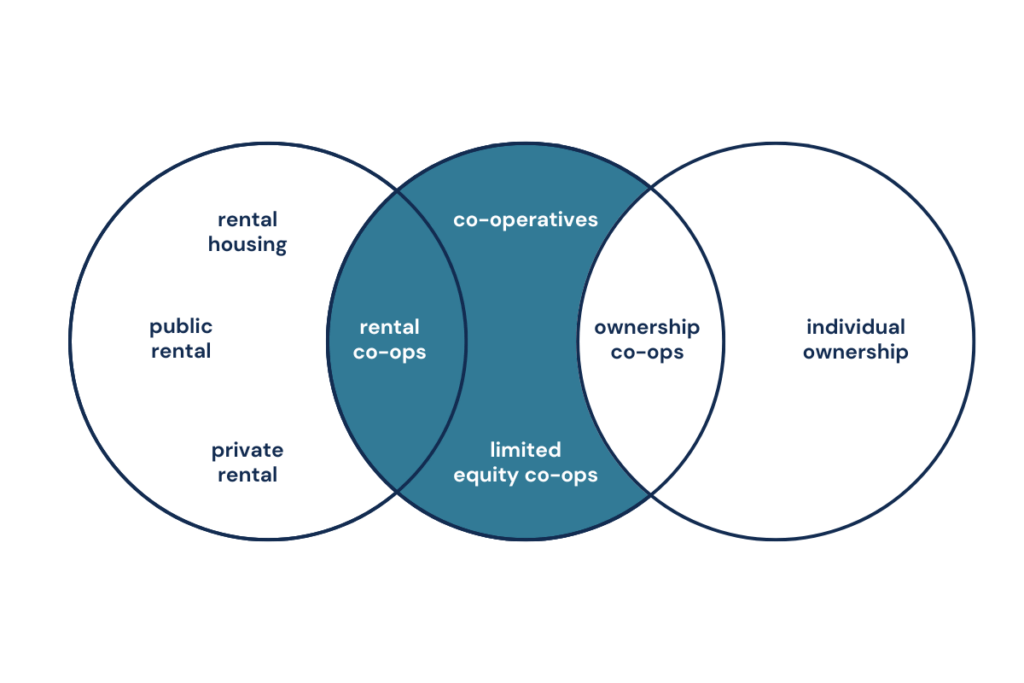

Housing co-operatives are a middle way, offering an alternative between owning and renting, as identified by this National Housing Supply and Affordability Council infographic.

Here are two types of housing co-operatives that fulfil the intermediate tenure model: rental and limited equity co-ops.

Lessons learned

In 2022, the BCCM supported the revitalisation of the Australian Co-operative Housing Alliance (ACHA), helping to develop a strategic plan for the rental housing co-operative sector, a website and advocacy materials. In April this year, we organised a study tour to Europe to learn from the co-operative housing sector there, producing a written report and recommendations for government. The key findings concluded:

- European housing co-ops exist at scale and are a mainstream housing option.

- Financing co-ops does not need ongoing subsidy when adopting government-guaranteed revolving loan schemes in partnership with private sector financial institutions and member contributions.

- Competitive tender and design processes ensures innovation, affordability and a social focus for housing and city development.

- Members’ active participation in decisions regarding their living and housing situation is a fundamental characteristic that ensures affordability and improved communities.

- European and Australian housing and financial systems are not fundamentally different, so adopting the best aspects of European co-ops for Australia is feasible.

An ARC-funded, five-year research project that published its findings in 2024 has also generated new evidence and visibility for housing co-ops in Australia.

The research found co-operative housing provides tenant–members with higher levels of housing stability, quality and security, and higher levels of agency and empowerment than other forms of rental housing. It also found co-op housing reduced costs due to higher levels of co-operative participation in tenancy and property activities.[9]

Research in Austria, where housing co-ops make up around 20 per cent of housing, found that co-ops have a significant impact on the overall housing market, in terms of both quality and rent. A 10 per cent increase in the share of co-op housing leads to about five per cent cheaper rents in the non-regulated rental sector, due to the price-dampening effect of at-cost co-ops.[10] This demonstrates the potential of housing co-operatives to play a significant role in re-shaping the Australian housing market with a tranche of housing that:

- is affordable in perpetuity (unlike subsidies to the private market)

- does not require ongoing government funding and can be self-funded

- is not as tightly targeted as social housing and can become mainstream

Further research in Austria demonstrated that the co-ops “are characterised by a distinct business model, based on the premise of cost-recovery and revolving funds. By deviating both from the logic of for-profit housing and from public housing, they occupy a distinct Third Sector role in Austria’s housing market”[11] that also improves overall societal prosperity.

In brief: “LPHA [limited-profit housing association] residents benefit from reduced housing costs, which in turn increases their purchasing power (after housing costs), which adds to GDP and reduces the need for housing allowances.”[12]

Housing co-ops only make up 0.05 per cent of the housing stock in Australia. The smaller co-operative housing sector in Australia is a result of historically high home ownership rates, meaning there was little need to develop an alternative. As house prices have risen faster than wages, the previously successful approach has faced market failure. In the absence of an alternative, Australians have been increasingly forced into insecure and unaffordable private-market rental[13] or homelessness.

In countries with higher proportions of housing co-ops, the “continuous expansion of limited-profit housing over previous decades … becomes particularly visible now at a time of increased pressures in the housing market, they have served to guarantee affordable and secure rents in perpetuity, against the unpredictable and volatile nature of housing markets.”[14]

Refining the focus: The BCCM’s role

Co-operative and mutual enterprises (CMEs) operate across all stages of the housing supply chain, made up of planning and development, construction finance, building, mortgages and housing management.

Examples of BCCM members’ roles across the supply chain:

- Mutual building groups are housing developers, such as Common Equity co-op companies or Property Collectives[15].

- Finance mutuals loan money for housing construction and for mortgages, including shared equity financing such as Bank of Us partnering with the Tasmanian Government on the My Home Program[16] and Police Bank partnering with the HOPE Housing[17] not-for-profit model.

- Housing co-operatives are providers in the management of affordable housing, with models that span co-ops in the social housing sector to those that are autonomous[18].

- Co-ops and mutuals, such as agricultural and social care co-ops, require affordable housing in order to secure essential workers in regional/remote and urban areas.

The BCCM undertook consultation with members from the finance mutual sector and the housing co-operative sector on the strategic direction for the BCCM in housing affordability. The results follow.

Summary of input from finance mutual members

Finance mutual members focused on the importance of collaborative funding pools and leveraging mutuals’ strengths to create sustainable, community-focused financial structures. There was an emphasis on the need to understand and work with regulation that facilitates investment in affordable housing. For example, models such as the one developed by KeyInvest that facilitates investment in housing by mutual banks.

Finance mutuals discussed the challenges and opportunities for attracting capital for shared equity models. Participants agreed on the need to involve superannuation funds by addressing liquidity concerns and creating structures aligned with regulatory frameworks. They additionally noted the need for innovative funding mechanisms and collaborative efforts to attract investment and support affordable housing initiatives.

This input generally points to a role for the BCCM in fostering collaboration, networking and relationships between members seeking to innovate.

Summary of input from housing co-op members

Members agreed there is a need to develop a cohesive narrative on how co-operatives and mutuals play a crucial role in addressing housing affordability. Raising awareness about the benefits of co-operative housing models and advocating for enabling government policies is crucial.

Increased collaboration among BCCM members, including cross-sectoral partnerships, is essential to find innovative solutions to the housing crisis. The BCCM strategy should align with broader government initiatives such as the Housing Australia Future Fund to maximise impact.

European co-operative housing models, where diverse funding sources and supportive policies have facilitated successful housing initiatives, can inform strategies for improving co-operative housing financing and policy in Australia.

This input indicates a role for the BCCM in advocacy, promotion and fostering collaboration – both between BCCM members seeking to innovate, and between BCCM members and government initiatives.

Timeline of key BCCM actions to date

September 2022

BCCM worked with ACHA to re-establish the organisation, providing secretariat support

December 2022

BCCM became Australian representative to Co-operative Housing International, a branch of the ICA. Australia was previously unrepresented

2022–2023

Finance mutual meetings to explore potential models

2023

Provided ACHA with digital infrastructure

April 2024

BCCM Study tour of European housing co-ops

November 2023

BCCM National Housing Roundtable, Parliament House (Canberra)

2022–2024

Submission to national and state housing enquiries

2024

NSW Parliamentary Housing Roundtable

2023–2024

Semi-regular meetings with state and federal housing ministers and various local government representatives about housing co-operatives

February 2024

Federal Minister for Housing attended opening of Lakewood co-operative housing in Melbourne

February 2019

Articulating Value in Co-operative Housing: International and Methodological Review released after commissioning by housing co-op bodies

March 2024

Release of the Value of Housing Co-operatives in Australia research paper by Western Sydney University, a cross-university, ARC-funded research over five years, sponsored by BCCM member housing co-op organisations

2024

Communication with AHURI about sector consultation in research about co-ops

2017

BCCM research paper produced on state of the co-op housing sector

2023

Submission to the development of a National Housing and Homelessness Plan

2023

Middle Ground housing feasibility study released, supported through the Bunya fund

July 2024

BCCM published authoritative paper on size of the housing co-op sector

August 2024

Handbook for setting up a Community Land Trust as a co-op released by Co-operation Housing (WA) after support from the Bunya fund

Impact

Our work has had significant impact, increasing the knowledge of decision-makers about co-operative housing and securing engagement from the media and the research community:

- Co-operative housing is back in the federal housing plan in The State of the Housing System 2024, the first report of the National Housing Supply and Affordability Council.

- Co-operative housing has featured in the media, including the SMH, SBS and The Project.

- There has been consultation from the Australian Housing and Urban Research Institute (AHURI) on research, following an approach from the BCCM and ACHA.

Analysis

Private rental investment cannot deliver housing for all members of the community in need, due to the gap between the cost of supplying new housing including profit, and the rent-paying capability of the residents. Australia is missing a class of housing that operates at cost and is accessible to middle- and low-income households. In other countries, this niche in the housing market is met by co-operatives.

Co-operative housing development models can boost housing supply by:

- Reducing costs: An owner or user-led model of development does not require a developer profit margin for projects to proceed. These models are intentional, deliberative and not speculative.

- Shaping markets: The growth of lower-cost co-op models of development and tenure drive competition between business models, encouraging all models to reduce costs for end users.

Ownership must be a focus in any discussion of housing affordability and security. BCCM members have indicated lack of access to housing impacts all co-operative and mutual sectors:

- Co-op and mutual employers are impacted by workforce shortages related to housing availability.

- Regional co-ops are often leaders in their region and have a desire to support housing accessibility for their community’s wellbeing.

- Many co-op and mutual members, as part of the broader population, struggle to secure affordable housing.

Millions of Australians could benefit from sustainable affordable housing with the agency of ownership through housing co-operatives, like those in many parts of Europe.

Finance mutuals have a history of driving accessibility of housing and are the natural leaders to generate this new class of housing in Australia, just as finance mutuals have done in other countries. The housing co-operative movement are the natural leaders for providing the solution to ownership, with the intermediate tenure, rent-like-you-own model.

Growing a mainstream intermediate tenure affordable housing class in Australia benefits all Australians and BCCM members as well as aligning to our 5-year strategic goal for co-ops and mutuals to be recognised for their potential to address key challenges facing the nation.

Conclusion and next steps

The BCCM has dedicated significant resources to support the co-op housing sector and improve awareness of the benefits co-op housing over the last few years. Our focus can now shift to supporting the sector to grow, innovate and promote itself (i.e., from enablement to facilitation).

The BCCM will continue to leverage our leadership as the key advocate for policy reforms benefitting co-ops and mutuals in all sectors. This will help ensure housing co-ops and financial mutuals can compete on a level playing field with other housing developers and funders.

Over the next three years the BCCM will prioritise work in these areas:

| What we will do | How we will do it | Why we will do it |

| Engage key decision makers

|

Support members and other proponents of co-op housing in political advocacy, policy reforms, media engagement and research.

Advocate for election commitments, policy inclusion of co-op housing and recognition of co-op membership as a form of ownership. Support the development of finance solutions for investment in co-op housing and other forms of affordable shared equity housing. |

To influence key decision makers for support to grow the co-op housing sector.

To support financial mutuals to meet market demand for affordable housing. |

| Engage media

|

Support members to highlight co-op housing benefits and promote news about co-op housing through mainstream and social media channels. | To increase awareness of housing co-operatives and their role in addressing affordable housing needs. |

| Support research

|

Support further research on the benefits of co-op housing, including consumer demand and financial modelling, to incentivise investment in co-op housing.

Use the BCCM resource library as a clearinghouse for current research, including the authoritative database on the size of the Australian co-op housing sector. |

To build an evidence base for co-op housing and ensure research informs advocacy efforts and policymaking.

|

| Sector organising and network building

|

Bring BCCM members with an interest in affordable housing together to facilitate innovation and to discover mutual solutions to the housing crisis.

Encourage co-operation between members to address the housing crisis including through finance and investment. |

To strengthen the co-op housing sector, foster innovation and collaboration. |

What success looks like

- One or two co-op housing developments are partially funded by the mutual sector by 2030 to demonstrate success and provide replicable models.

- The proportion of co-operatives in community housing increases from 3.5 per cent to 10 per cent.

- A dedicated funding stream for co-op housing is reinstated in federal housing programs (e.g. HAFF).

- Regulatory settings do not inhibit financial mutuals investing in affordable housing on a competitive footing with other forms of institutional capital.

- Research on the benefits of co-op housing is widely disseminated and influences supportive housing policies.

- Australia gains international recognition for its co-operative housing sector.

Report notes

[1] “Affordable housing” is defined as housing that costs less than the “housing stress” threshold i.e. 30 per cent of income for very-low to medium-income households).

[2] ABS Census data, Judith Yates, special request tabulations, found ‘More rented, more mortgaged, less owned’ The Conversation 2022. Data excludes ‘not stated’.

[3] KPMG (2023) Value in Numbers: Measuring the impact of customer-owned banking.

[5] BCCM data

[6] National Housing Supply and Affordability Council (2024) State of the Housing System.

[7] Apps, A. (2021). The Limited Equity Housing Co-operative. Australian Property Law Journal, 29.

[8] www.moba.coop

[9] Crabtree-Hayes, L., Ayres, L., Perry, N., Veeroja, P., Power, E. R., Grimstad, S., Stone, W., Niass, J., & Guity, N. (2024). The Value of Housing Co-Operatives in Australia. https://doi.org/10.26183/0xpp-g320

[10] Klien, M., Huber, P., Reschenhofer, P. (WIFO), GutheilKnopp-Kirchwald, G., Kössl, G. (GBV). (2023). The Price Dampening Effect of Non-profit Housing. Austrian Institute of Economic Research (WIFO), Austrian Federation of Non-Profit Housing Associations (GBV).

[11] CIRIEC Working Paper. (2022). The system of limited-profit housing in Austria: cost-rents, revolving funds, and economic impacts.

[12] Klien M., & Streicher, G. (2021). The economic impacts of Limited-Profit Housing Associations in Austria WIFO – Austrian Institute of Economic Research.

[13] Apps, A. (2021). The Limited Equity Housing Co-operative” Australian Property Law Journal 29

[14] Klien M., & Streicher, G. (2021). Ibid.

[15] https://propertycollectives.com.au/building-groups/

[16] https://bankofus.com.au/my-home

[17] https://hopehousing.com.au/

[18] Baiges, C. et al 2019 International policies to promote cooperative housing La Dinamo Fundacio.

Latest campaigns

The Power of Co

Blueprint for Australia