05 October 2016

Australian mutual institutions collectively make up a $98.7 billion sector that represents the “fifth pillar” of banking in Australia – the fifth largest holder of household savings deposits in Australia. And with more than 4 million members already, this sector sees growth of 6.6% per year.

Apparently, more Aussie families are taking out home loans with customer-owned institutions than ever before, with customer-owned loans growing at more than double the rate of the Big 4 as of March 2016 (Customer Owned Banking Association – COBA).

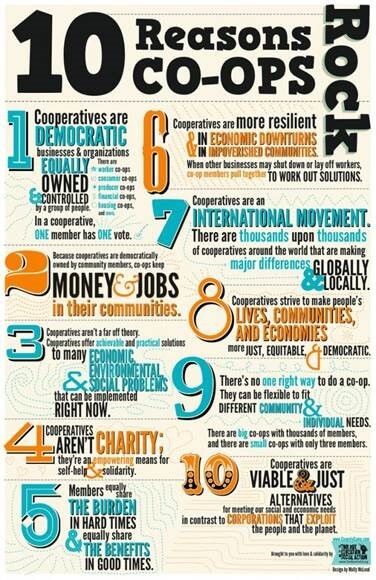

Co-operatives are autonomous associations formed and democratically run by people who come together to meet common economic, social and cultural needs.

They are founded on the principle of participatory governance, co-operatives are owned by those who use their services: their members.

What is customer owned and mutual banking?

Customer-owned banking and mutual banking mean the same thing – a financial institution that is owned by its members.

Where they differ from banks is that their customers own the bank – and as such are at the centre of everything they do.

One customer gets one member share, which is equal on constitutional matters affecting the customer-owned bank.

Profits are reinvested back into the products and services offered by the customer-owned bank, rather than being distributed to shareholders as a dividend.

A recent Canstar Blue survey of 1,898 customers of challenger and customer-owned banking institutions found that an impressive 83 percent of customers are highly satisfied with their institution of choice and only 2 percent of respondents were dissatisfied.

Many types of financial institution fall under the “customer-owned banking” banner:

- Mutual banks

- Credit unions

- Building societies

Australian customer-owned institutions provide generally the same consumer banking services as listed banks are Authorised Deposit-Taking Institutions (ADIs), regulated under the Banking Act.

This means that, while smaller in size, customer-owned institutions still meet the same high standards of prudential regulation as banks with full regulatory oversight – and are underwritten by the Australian government.

What is the difference between a co-operative and a mutual enterprise (CMEs)?

A mutual, mutual organisation or mutual society is an organisation (which is often, but not always, a company or business) based on the principle of mutuality. Unlike a true co-operative, members usually do not contribute to the capital of the company by direct investment, but derive their right to profits and votes through their customer relationship.

Where can I find mutuals to switch to?

Canstar

COBA

Members Own Health Alliance

BCCM members

What is a co-operative or mutual?

BCCM pusiness planning

The Co-operative Group (UK)

About mutual banks in Australia

COBA

Videos

What is a Co-operative?

The Difference between Banks and Credit Unions: Part 1

More information

www.bccm.coop

www.ica.coop

Image source: picturesofmoney.org

Latest news

First international Accreditation of Mutual Value presented

Finding senior leaders: A recruitment guide for co-ops and mutuals – Part 3